Context-Based Metrics is the meeting point between Science- and Ethics-Based Metrics.

Source: Sustainable Brands.

Source: Sustainable Organisations.

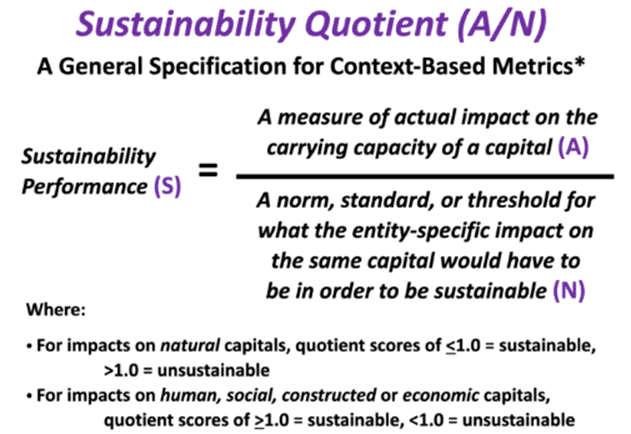

- In the context of environmental metrics, greenhouse gas emissions of a company (numerator) will be measured against the science-based reduction targets (denominator) tied to the reversal of climate change and the stabilisation of GHGs in the atmosphere to safe levels.

- When it comes to social context, an example would be corporate gender diversity (numerator) measured against a norm of more than 40 percent of either gender on a board of directors (denominator).

- In the economic context, return on equity could be measured against earnings sufficient to cover the cost of capital employed in a particular project.

- Launch/Orient CSM Function – Involves establishing conceptual commitments according to the carrying capacities of vital capitals for stakeholder wellbeing. This step also involves considering the impact to the triple bottom line. It involves choosing an approach that is context-based and not incremental.

- Identify Stakeholders – Identifying parties to whom the organisations actions will have an impact on (both human and non-human). This process also involves making sure all stakeholders are considered and defining to whom a duty or obligation is owed.

- Set Standards of Performance – Setting standards for an organisation is a function of its impact on the carrying capacity of vital capitals to ensure stakeholder wellbeing. Metrics must be developed to manage impacts on each stakeholder group identified in Step 2.

- Measure/Assess Performance – Measurement of the individual organisation (numerator in the Sustainability Quotient) must take place against the norms and standards set in Step 3 (denominator in the Sustainability Quotient). This process provides numerical sustainability performance scores and measures the gaps between actual performance and normative performance. This process be a proactive and continuous process.

- Plan Strategies and Interventions – Where gaps are discovered in performance, corporate sustainability strategies must be developed to bridge the gaps.

- Implement Strategies and Interventions – Strategies developed in Step 5 must be implemented in order to maintain the standards set in terms of the carrying capacity of the vital capitals to ensure stakeholder wellbeing.

Corporate Sustainability Management Cycle.

Source: McElroy and Van Engelen, 2012.

- SDG 6: “Clean Water and Sanitation“. Context-based metrics can assess and address water usage in a specific context, considering local availability and needs.

- SDG 7: “Affordable and Clean Energy“. Organisations using context-based metrics may tailor their energy consumption and efficiency measures based on local energy availability and accessibility.

- SDG 8: “Decent Work and Economic Growth“. Applying context-based metrics allows for the assessment of social and economic impacts of organisations on local communities, ensuring the alignment of employment practices with the relevant context.

- SDG 12: “Responsible Consumption and Production“. Organisations adopting context-based metrics can evaluate their resource consumption and production practices in a way that is sustainable within the specific context.

- SDG 13: “Climate Action“. Organisations can use context-based metrics to assess and mitigate their environmental impact, taking into account local climate conditions and vulnerabilities.

- SDGs 14 and 15: “Life Below Water” and “Life on Land“. Context-based metrics may be relevant for organisations operating in specific ecosystems, helping to ensure sustainable land use practices.